Australian Industires facing Cash Flow Contraction

The Australian economy is holding up pretty well overall, but when you look closer, there’s a serious squeeze happening in specific small and medium-sized businesses (SMEs) right across Australia, especially in places like Melbourne and Victoria. This period is defined by a double whammy: persistent, tight monetary policy keeping interest rates high, coupled with deep seated operational inflation impacting crucial inputs like labour and materials. These factors are severely eroding the operating margins of vulnerable firms, leading to a critical normalisation—or, in many cases, total depletion—of the cash reserves that businesses managed to accumulate during the pandemic years.

The problem across the country, especially for these firms, is fundamentally one of liquidity, not necessarily systemic solvency. The increase in corporate insolvency, while concerning, is concentrated in small firms that typically hold little traditional bank debt. However, these failures are preceded by a critical breakdown in short-term financial health, manifested as sizable operational debts, including overdue trade credit and outstanding tax obligations like GST. This signals an acute failure in the essential management of day-to-day capital, known as working capital.

For businesses caught in this contraction, traditional debt financing often isn’t the right fix or is simply inaccessible, particularly when their balance sheets are already stretched or their credit profile is weak. As specialists in SME Business Accounting and Tax in Australia, SEED PLUS is all about delivering agile, non-debt liquidity solutions, such as invoice factoring, which are specifically designed to bridge these short-term liquidity gaps and restore a consistent cash flow stream without piling on more debt.

The depletion of cash buffers serves as the primary trigger for the current spike in insolvencies. During the period of pandemic stimulus and reduced operational costs, many businesses built up significant cash reserves. As inflation accelerated and interest rates increased, these temporary reserves were rapidly consumed. Once this financial buffer is exhausted, the combined weight of high interest costs and slower consumer demand immediately translates into insolvency. This shows that the perceived resilience of many smaller firms was fragile and highly dependent on those temporary cushions. Consequently, the businesses currently entering distress are acutely sensitive to even minor cash flow fluctuations, meaning they urgently need targeted interventions.

I. Financial Challanges: Why Australian SMEs are Struggling

Australia’s economic landscape is marked by unique challenges, creating a highly demanding operating environment for SMEs, with these trends often amplified in major hubs like Melbourne, Sydney and now in Brisbane, Adelaide and Perth.

A. The Macroeconomic Squeeze: Rates, Inflation, and Demand

The Australian economy continues to navigate the pressures of high interest rates and inflation. Restrictive monetary policy has directly impacted SME financials by making debt servicing significantly more expensive, especially for firms relying on variable rate loans or those mandated to refinance existing facilities. This process diverts cash flow away from productive use such as covering day-to-day expenses or investing in working capital and into debt service.

Simultaneously, persistent input cost inflation remains a dominant pressure. Costs related to wages, utilities, and construction materials remain elevated. Where businesses operate in competitive markets, they often cannot pass these increased costs directly to consumers or clients, leading to severe margin compression. This pressure is particularly pronounced in Victoria, where the state government has noted challenges related to slowing productivity in conjunction with elevated rates.

The current elevated insolvency rates, particularly in the most affected Australian sectors, are not purely a signal of unprecedented economic collapse, but partly represent a post-pandemic adjustment. Insolvency levels are performing a “catch-up” following an extended period of artificial lows during government intervention. This signifies a return to a more challenging, competitive equilibrium where firms must rely entirely on their intrinsic financial resilience.

B. The Structural Vulnerability of the SME Business

The specific nature of the business failures indicates a major structural vulnerability in the small business sector. Data confirms that high cash buffers built during the pandemic across SMEs have generally returned to “more normal levels,” directly preceding the observed normalisation of company insolvency rates across most industries.

While these insolvencies limit broader spillovers to the financial system because the firms involved are typically small and carry little bank debt , the microeconomic pain is profound. Many of these small businesses have accumulated sizable operational debts. These liabilities include overdue trade credit (delayed payments to suppliers) and unpaid GST collected on behalf of the government. The accumulation of non-bank operational debt suggests that the core financing challenge is not securing long-term capital expenditure, but rather immediate, short-term working capital liquidity.

When a small business resorts to using collected GST or delays paying critical suppliers to fund daily operations, it is essentially self-financing its own failure. This practice is fundamentally unsustainable and acts as a critical precursor to formal insolvency. A firm in this position is typically disqualified from traditional bank loans due to perceived risk but presents a perfect use case for non-debt liquidity solutions that specifically address the gap in the accounts receivable cycle.

II. Australia’s Five Industries facing challanges

Based on recent RBA reports detailing concentrated stress and ASIC insolvency data, three core sectors Construction, Retail, and Hospitality are consistently identified across Australia as having elevated insolvency rates due to persistent cash flow challenges and thin operating margins.

5 Industries Facing the Toughest Cash Flow Headwinds (Reflecting National Trends):

- Residential and Small-Scale Construction

- Commercial and Industrial Building Construction

- Discretionary Retail

- Hospitality and Accommodation Services

- Transport, Postal, and Warehousing

III. Cash Flow Crisis

The following detailed analysis explores the specific operational and structural vulnerabilities driving the cash flow crises within each of the five critical sectors in the Australian market.

Residential and Small-Scale Construction

This sector remains the engine of Australia’s insolvency spike and is severely impacted by twin pressures. The primary headwind is the devastating combination of margin compression and fixed-price contract traps. Many smaller builders, operating on thin margins, locked in contracts before the major inflationary surge began, forcing them to absorb drastically higher material and labour costs, a situation that has driven many to failure.

The key structural weakness is high exposure to trade credit and delayed payments. The RBA specifically noted that smaller firms in the construction industry accumulated significant overdue trade credit in recent years. This means that even successful Australian builders are often facing massive liquidity gaps created by slow payment cycles from clients or larger developers, preventing them from paying sub-contractors or suppliers on time. The cash conversion cycle has lengthened drastically, turning profitable projects into cash flow disasters.

Commercial and Industrial Building Construction

This segment of construction faces a different but equally destructive pressure: systemic market contraction. According to industry analysis, the sectors related to private investment are undergoing a significant pipeline reduction. Forecasts show that the Factory and Industrial Building Construction industry is expected to face a revenue decline of -18.9% in the coming years, while the broader Commercial and Industrial Building Construction is forecast to decline by -9.7%.

This primary challange means that for many Australian SMEs dedicated to non-residential projects, future work is simply becoming scarcer. The key structural weakness is the inherent reliance on large, intermittent payments linked to project milestones. In a shrinking market, financing these gaps becomes exponentially harder, as traditional lenders grow increasingly cautious about providing liquidity to a declining sector. While governments are focused on driving economic growth through infrastructure , the national downturn in private industrial investment means local firms relying on commercial contracts are facing a severe, structural demand shock.

Discretionary Retail

Australia’s discretionary retail sector is inextricably linked to household budgets. The primary challange is a sharp decline in consumer demand driven by the interest rate shock. As households prioritise essential spending and servicing mortgages and utility bills over non-essential items, retail revenues fall.

The key structural weakness involves high fixed overheads (especially in cities like Melbourne) coupled with inherent inventory risk. Retail requires substantial working capital for stock acquisition long before sales are realised. If demand is subdued, inventory sits unsold, locking up capital and drastically lengthening the cash conversion cycle. Elevated insolvency rates are confirmed in this sector, particularly affecting the smaller, independent shops that characterise inner-city and suburban strips across the country.

Hospitality and Accommodation Services

As a highly labour-intensive sector, Hospitality faces extreme pressure from wage inflation and soaring operational costs, squeezing already thin margins. This is the primary headwind—the inability to raise prices sufficiently to offset runaway costs without alienating price-sensitive customers.

The key structural weakness is twofold: reliance on volatile, transient demand and fragile balance sheets stemming from the recovery period. Many small firms in this sector accumulated tax arrears (GST) and overdue trade credit during the pandemic and recovery phase, which now act as destabilising debts as government support ends. For cities like Melbourne, which rely heavily on events and culture , the high operational turnover and low margins mean liquidity crises can materialise rapidly, forcing smaller cafes, restaurants, and independent accommodation providers into insolvency.

Transport, Postal, and Warehousing

While the national data for the broader Transport, Postal, and Warehousing industry showed a significant increase in Operating Profit Before Tax (OPBT) recently , this aggregate national figure is often misleading when assessing localised SME financial health. For Australian SMEs in this sector, the primary challange is volatility driven by its dependence on the deeply distressed feeder industries Construction and Retail.

The key structural weakness is high exposure to bad debt and long payment terms from struggling clients in construction and retail, creating a detrimental ripple effect across the supply chain. Furthermore, this sector relies heavily on capital assets (vehicles, machinery), meaning debt taken out for capital purchases pre-rate hike is now significantly more expensive to service. The simultaneous failure of smaller construction and retail firms translates localised liquidity losses for logistics SMEs, often through non-payment or default on large invoices.

The confluence of specific sectoral distress reveals that the insolvency spike is not merely a general economic downturn but a targeted crisis of Accounts Receivable and Accounts Payable management within these high-risk industries. Since many distressed firms have low bank debt but high operational arrears , their failure stems from the inability to convert sales into immediate cash quickly enough (long accounts receivable cycles), exacerbated by high input costs (high accounts payable). This dynamic solidifies the necessity for solutions that prioritise optimising the debtor book.

IV. Proactive Cash Flow Optimisation

For Australian SMEs operating in these challenging sectors, the primary focus must shift from growth strategies to survival strategies—specifically, managing debt exposure and accelerating the cash conversion cycle. Proactive financial management is the critical first step before seeking external funding.

Internal Financial Discipline

Robust cash flow forecasting mastery is now non-negotiable. Businesses must shift beyond simple Profit & Loss tracking and implement detailed, 13-week rolling cash flow forecasts to predict and mitigate shortfalls proactively. This allows management to anticipate liquidity needs well in advance, rather than reacting to crises.

Simultaneously, an aggressive cost and margin analysis must be undertaken. This involves a comprehensive review of all operating expenses, particularly focusing on optimising the cash conversion cycle. For highly labour-intensive sectors like Hospitality and input-heavy sectors like Construction , optimising supplier payment terms and streamlining internal processes to reduce waste can significantly preserve capital. When interest rates are high, the opportunity cost of having slow-paying invoices or excessive debt exposure increases dramatically; capital tied up in delayed receivables is costing the business more in debt servicing every day.

Debt Restructuring and Review

SMEs holding variable-rate loans must urgently explore refinancing options to stabilise monthly payments. Where feasible, refinancing into fixed-rate structures provides a crucial hedge against the possibility of future interest rate hikes, offering stability in monthly debt service obligations. Businesses may also explore negotiating longer loan terms to reduce immediate monthly payments, although this must be balanced against the increased total interest paid over the life of the loan.

Furthermore, prudent new borrowing is essential. In a high-rate environment, management should rigorously assess whether planned expansions or large purchases are genuinely urgent or if they can be delayed until rates stabilise or drop. Taking on new, high-interest debt for non-critical expansion only exacerbates existing cash flow strain.

V. The Solution to Short-Term Liquidity

As traditional banks tighten lending criteria and focus primarily on companies with minimal exposure to high-risk sectors , alternative financing solutions become essential for Australian SMEs. SEED PLUS specialises in bridging the gap between cash flow pain points and long-term business viability.

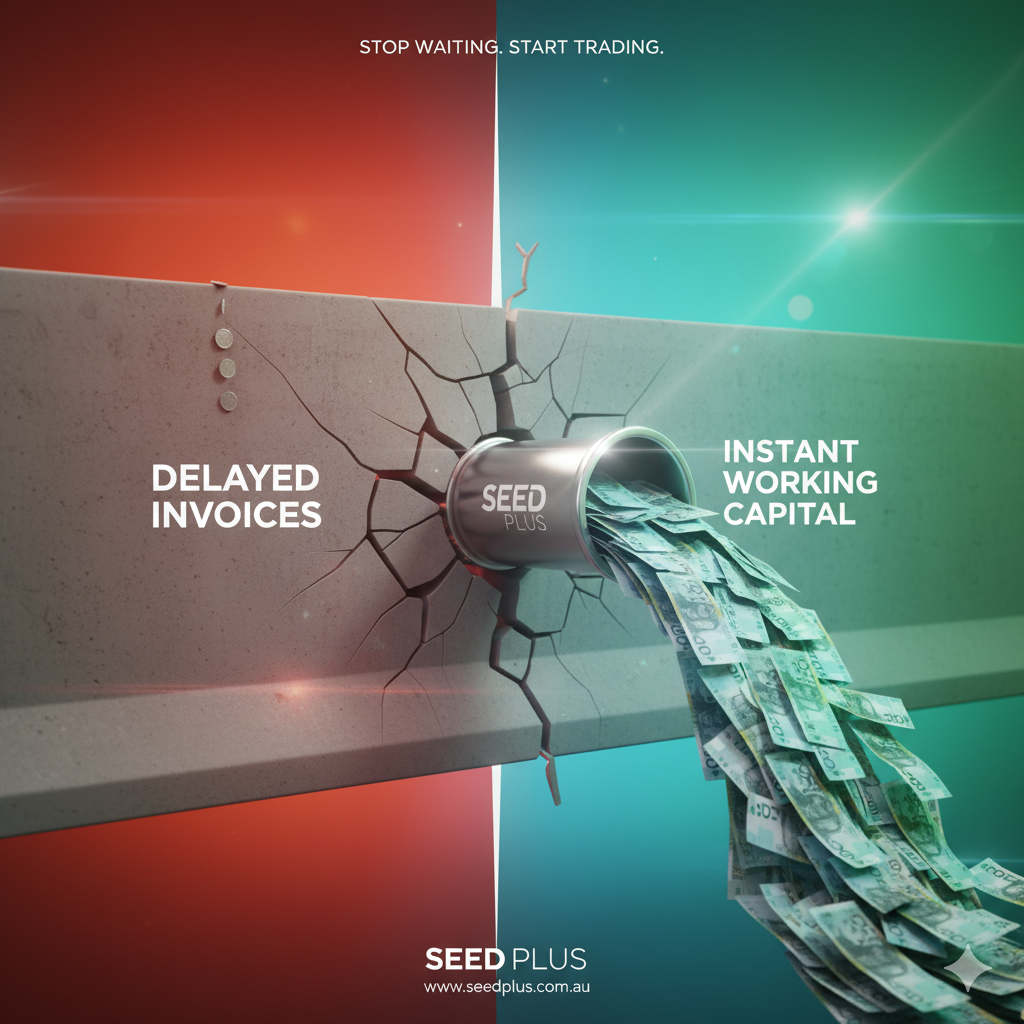

Invoice Factoring: Non-Debt, Asset-Based Liquidity

For the majority of the five distressed industries, the crisis is one of delayed receivables. Invoice factoring—a powerful non-debt solution—directly addresses this issue.

Factoring is the sale of a business asset (its accounts receivable or invoices) to a third party, the factor, in exchange for immediate cash. This is critical for SMEs already burdened by high interest rates, as factoring does not incur new debt or compound existing liabilities. For Construction and Transport SMEs, this process instantly converts overdue trade credit into working capital, allowing them to meet payroll, cover material costs, and avoid accumulating debilitating arrears.

A key advantage for Australian SMEs with less-than-perfect internal credit scores is that factoring companies assess risk primarily based on the customer’s (the debtor’s) creditworthiness, not the borrowing business’s. This significantly increases the chances of approval for firms facing financial stress but who serve established, creditworthy clients. Factoring provides rapid access to funding with less paperwork compared to traditional funding methods, making it an agile choice for firms needing prompt relief.

‘Capital Plus’ Approach

Beyond immediate liquidity needs, SEED PLUS’s expertise also extends to seed finance, which is crucial for early-stage enterprises in high-growth Australian sectors, including those thriving in Melbourne like Digital Technology or Life Sciences , that might eventually face volatility. Seed finance is the initial capital used for solution and business-model development before a company achieves proof of concept or begins generating revenue.

Building Resilience with SEED PLUS

The current financial environment presents a concentrated threat to operational cash flow within Australia’s key functional industries, with these pressures heavily felt in Melbourne: Residential Construction, Commercial Construction, Discretionary Retail, Hospitality, and Transport. The challenges in these areas are fundamentally liquidity crises, often driven by operational debt, delayed receivables, and depleted cash buffers, rather than broad systemic bank instability. Timely and targeted financial intervention is therefore essential for survival.

Proactive working capital management is the critical factor differentiating survival from insolvency. Relying solely on traditional bank lending in a tightening credit market exposes these already vulnerable businesses to higher interest costs and stricter lending criteria.

SEED PLUS offers a critical pathway to stability by providing fast, non-debt liquidity solutions. Invoice factoring, in particular, directly addresses the accounts receivable failures prevalent in sectors like Construction and Transport, converting the tangible value of a company’s sales into immediate operating cash. For Australian businesses seeking stability through business finance, exploring alternative funding mechanisms like asset-based financing or targeted business finance represents the most resilient strategy against current and future economic challanges. SEED PLUS is positioned to be the essential partner for businesses seeking to stabilise their finances, optimise their cash flow cycles, and move from crisis management to sustainable growth.

Disclaimer

This blog post is for general information only. It’s not financial or legal advice. Every business is different, so what’s right for one might not be right for another. You should always get advice specific to your own situation from a qualified professional. We are giving general information only.

Need a Hand with Your Business Growth?

SEED PLUS is located in Rowville Melbourne, Victoria, and want to talk more about challanges your business is facing, restructuring or cash flow issues or to tidy up your books, in making your business more profitable, then SEED PLUS can help. We’re an experienced Accounting Practice, operating more than 15 years, and we understand the numbers and the rules.

Contact SEED PLUS today! Let’s make your business shine, not just in profits, but in positive impact on the socity, environment and economy too.

Contact our office: (03) 6153 0180 to discuss your scenario.